Who wins when AI works?

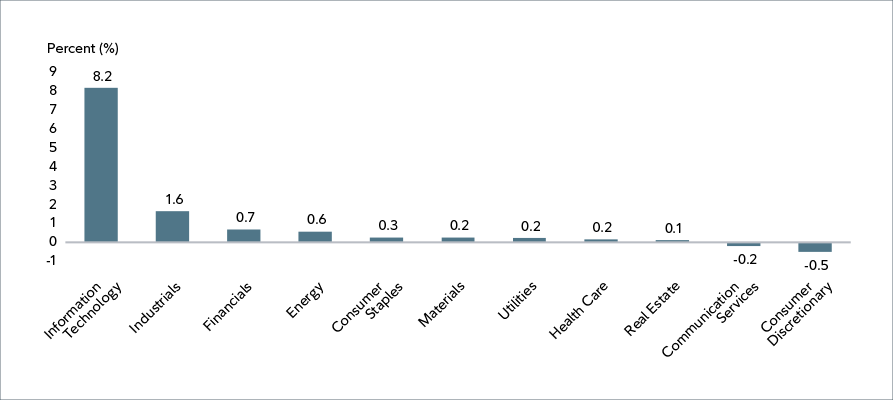

The AI trade remained in control of equity markets through the first half of 2026, with stocks performing strongly despite volatility owing to the Iran war. The MSCI All Country World Index returned 11%, with the tech sector accounting for the vast majority of that (see Exhibit 1). 19 of the top 20 individual contributors to the ACWI return were all tech companies.

EXHIBIT 1: MSCI ACWI contribution to total return

Source: Fidelity, year-to-date ending June 30, 2026.

Our approach to the AI trade in the multi-asset funds for which we’re responsible remains twofold. First, we continue to be guided by the bottom-up signals from our research analysts who know these companies and sectors inside and out; so long as they keep telling us that the market is underestimating the earnings power of these companies (which they continue to), we will be inclined to maintain a tactical overweight to equities. Second, we are ensuring that we keep capital with our equity managers who we believe are best placed to pick the individual winners and avoid the losers, while calibrating our overall market exposure using futures positions to achieve what we think is the appropriate aggregate risk posture.

Our top-down research agenda remains focused on the implications of AI on the macro drivers of longer‑term returns across asset classes – economic growth, productivity, inflation and interest rates. As with past big technological innovations, the direct implications of AI centre around productivity growth. Guided by the experience of those past innovations, our researchers estimate that overall productivity growth in the US may ramp up by close to 1% per year (AI: An X-factor in a new investment regime).

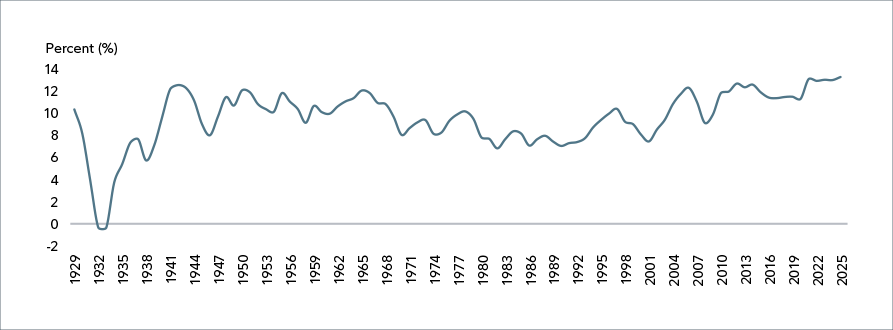

That’s a lot, as far as these things go. Trouble is, it doesn’t appear to be nearly enough to underwrite the kind of growth in profits now being discounted in lofty‑looking equity valuations. Our best judgment is that the US equity market is implicitly projecting roughly 10% real growth in earnings over the next few years, while the projected AI‑related boost in productivity would only take sustainable real GDP growth up from about 2% to 3%. Companies are already taking a record share of the overall economy’s income; the capital-labour ratio, as proxied by corporate profits as a share of GDP, stands at its highest level in the 90 years of data we have available in the US (see Exhibit 2). So, for the equity market to be right, companies will have to take a larger share of the economy’s income than we’ve ever seen before.

EXHIBIT 2: US corporate profits as a share of GDP

Source: Haver analytics as of December 31, 2025

On its face, that’s an aggressive assumption. The capital‑labour ratio has tended to be a fairly stable variable over a long period of time. This is despite both cyclical booms and busts and structural changes brought about by waves of technological innovation.

A main reason for that broad stability in the capital‑labour ratio seems to be that technological innovations – from railroads to electrification to telephones to computers – have generally followed a similar pattern. As adoption ramps up, new technologies enable higher productivity, both helping existing workers do their jobs better and displacing workers into new, more productive roles. That latter process is never smooth, to be sure, but has always eventually worked itself out, resulting in a fully employed labour market. Overall, competition among firms and workers, and bargaining between them, tends to ensure that the economic gains are split between profits and wages – or in other words, between the owners of capital and the providers of labour.

One of the key features of these prior waves of innovation is that the technologies have tended to be complementary, in the sense that they ultimately make people more productive. For example, we’ve always needed drivers for modes of transportation, whether a horse-drawn carriage or a train or a transport truck.

But maybe no longer, which is why this time may in fact be different. AI appears to be more of a replacement technology than anything we’ve seen before. Rather than making the entire workforce more productive, AI may obviate the need for a potentially significant number of workers in many sectors of the economy. Prior technological innovations tended to complement labourers while replacing relatively few, and temporarily so at that. AI on the other hand may replace labour, and complement only those managing the AI, potentially forever. As a result, the productivity gains from AI would tend to accrue largely to companies and those select managers.

If the owners of the AI indeed don’t have to share as much (or any) of its productive fruits with workers, the capital-labour ratio should rise. Corporate profits in the US currently stand at 13% of GDP. The market seems to be implying an increase to the high teens over the next few years. But if AI is truly more of a replacement technology than anything we have seen before, why can’t it be 20%? Or 40%? Or 100%, as AI maximalists would probably have it?

As a result, the breakout in the capital-labour ratio implied by current market pricing may not be too aggressive; it may even be conservative. By implication, equities may not be overvalued in aggregate; they may be undervalued.

We can’t say which of these is right at this stage. We don’t think anyone can. But we can say two things with some confidence. One, the extent to which AI acts as a replacement technology rather than a complementary technology will be far more important to longer-term capital market returns than news on the latest batch of chip orders. And two, the assumption the equity market seems to be implicitly making on the potential for AI to become a replacement technology is not entirely implausible.

The distant future may be unknowable but it’s not entirely unresearchable. Our group is spending a lot of time on this issue, trying to understand the similarities and differences between AI and past technological waves, as well as closely scrutinizing profit margin and labour market dynamics to detect signs of a structural break in the way the economy functions. We are also trying to anticipate the response of government and regulators who will undoubtedly have a significant role to play in managing the distributional and geopolitical impacts of AI. In the meantime, as mentioned at the outset of this piece, our active allocation positioning remains largely reliant on our bottom-up earnings signals, since we believe it to be inappropriate to take a strong view on the nearly-imponderable top‑down issues.

Finally, let us note that as investors we care about AI because of its implications for the funds we manage. We manage those funds for people. And we know that for many people, one consequence of the emergence of AI that we’ve written about here is that it may represent more of a challenge than an opportunity. This leads to an argument for being invested in the capital of the owners of the AI – if people’s careers could be disrupted, better they own a piece of the thing benefiting from that disruption. We’d rather those people make those investments through our funds, of course, but even if not, it’s worth contemplating as we manage not only the market implications of AI but its broader implications for the way our world functions.

Authors:

David Wolf l Portfolio Manager

David Wolf is a Portfolio Manager for Fidelity Investments. He is the co–manager of Fidelity Managed Portfolios, Fidelity Global Equity+ Fund, Fidelity Global Equity + Balanced Fund, Fidelity Canadian Asset Allocation Fund, Fidelity Canadian Balanced Fund, Fidelity Monthly Income Fund, Fidelity U.S. Monthly Income Fund, Fidelity Global Monthly Income Fund, Fidelity Global Dividend Fund, Fidelity Income Allocation Fund, Fidelity American Balanced Fund, Fidelity Conservative Income Fund, Fidelity NorthStar®, Fidelity NorthStar® Balanced Fund, Fidelity CanAm Opportunities Class, Fidelity Inflation-Focused Fund, Fidelity Canadian Monthly High Income ETF Fund, Fidelity Global Monthly High Income ETF Fund and Fidelity Tactical Global Dividend ETF Fund. He is also portfolio co‑manager of Fidelity Conservative Income Private Pool, Fidelity Asset Allocation Private Pool, Fidelity Balanced Private Pool, Fidelity Balanced Income Private Pool, Fidelity U.S. Growth and Income Private Pool, Fidelity Global Asset Allocation Private Pool and Fidelity Global Asset Allocation Currency Neutral Private Pool.

David Tulk, CFA l Portfolio Manager

David Tulk is a Portfolio Manager for Fidelity Investments. He is the co manager of Fidelity American Balanced Fund, Fidelity Asset Allocation Private Pool, Fidelity Balanced Income Private Pool, Fidelity Balanced Portfolio, Fidelity Global Equity + Balanced Fund, Fidelity Balanced Private Pool, Fidelity Canadian Asset Allocation Fund, Fidelity Canadian Balanced Fund, Fidelity Canadian Monthly High Income ETF Fund, Fidelity Conservative Income Fund, Fidelity Conservative Income Private Pool, Fidelity Conservative Managed Risk Portfolio, Fidelity Global Asset Allocation Private Pool, Fidelity Global Balanced Portfolio, Fidelity Global Dividend Fund, Fidelity Global Equity Portfolio, Fidelity Global Growth Portfolio, Fidelity Global Growth Private Pool, Fidelity Global Income Portfolio, Fidelity Global Monthly High Income ETF Fund, Fidelity Global Monthly Income Fund, Fidelity Growth Portfolio, Fidelity Income Allocation Fund, Fidelity Income Portfolio, Fidelity Inflation-Focused Fund, Fidelity Monthly Income Fund, Fidelity NorthStar® Balanced Fund, Fidelity Tactical Global Dividend ETF Fund, Fidelity U.S. Growth and Income Private Pool and Fidelity U.S. Monthly Income Fund

Ilan Kolet l Institutional Portfolio Manager

Ilan Kolet is an Institutional Portfolio Manager for Fidelity Investments. In this role, Mr. Kolet serves as a member of the investment management team, maintaining a deep knowledge of portfolio philosophy, process and construction. He assists portfolio managers and their CIOs in ensuring portfolios are managed in accordance with client expectations.

Bruno Crocco, CFA l Portfolio Manager

Bruno Crocco is a Portfolio Manager for Fidelity Investments. He is the co–manager of the Fidelity ClearPath Retirement Portfolios, Fidelity ClearPath Institutional Portfolios and Fidelity ClearPath Index Plus Portfolios. He is also the co-manager of the Tactical Asset Allocation suite and other multi-asset strategies for Canadian investors.

Jon Knowles, CFA l Institutional Portfolio Manager

Jon Knowles is an Institutional Portfolio Manager for Fidelity Investments. In this role, Mr. Knowles serves as a member of the investment management team, maintaining a deep knowledge of portfolio philosophy, process and construction. He assists portfolio managers and their CIOs in ensuring portfolios are managed in accordance with client expectations.

Commissions, trailing commissions, management fees, brokerage fees and expenses may be associated with investments in mutual funds and ETFs. Please read the mutual fund or ETF’s prospectus, which contains detailed investment information, before investing. The indicated rates of return are historical annual compounded total returns for the period indicated including changes in unit value and reinvestment of distributions. The indicated rates of return do not take into account sales, redemption, distribution or option charges or income taxes payable by any unitholder that would have reduced returns. Mutual funds and ETFs are not guaranteed. Their values change frequently, and investors may experience a gain or a loss. Past performance may not be repeated.

The index returns are shown for comparative purposes only. Indexes are unmanaged, and their returns do not include any sales charges or fees as such costs would lower performance. It is not possible to invest directly in an index.

From time to time a manager, analyst or other Fidelity employee may express views regarding a particular company, security, and industry or market sector. The views expressed by any such person are the views of only that individual as of the time expressed and do not necessarily represent the views of Fidelity or any other person in the Fidelity organization. Any such views are subject to change at any time, based upon markets and other conditions, and Fidelity disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Fidelity Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Fidelity Fund.

Certain Statements in this commentary may contain forward-looking statements (“FLS”) that are predictive in nature and may include words such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “estimates” and similar forward-looking expressions or negative versions thereof. FLS are based on current expectations and projections about future general economic, political and relevant market factors, such as interest and assuming no changes to applicable tax or other laws or government regulation. Expectations and projections about future events are inherently subject to, among other things, risks and uncertainties, some of which may be unforeseeable and, accordingly, may prove to be incorrect at a future date. FLS are not guarantees of future performance, and actual events could differ materially from those expressed or implied in any FLS. A number of important factors can contribute to these digressions, including, but not limited to, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, global equity and capital markets, business competition and catastrophic events. You should avoid placing any undue reliance on FLS. Further, there is no specific intention of updating any FLS whether as a result of new information, future events or otherwise.

“Fidelity Investments” and/or “Fidelity” refers collectively to: i) FMR LLC, a US company, and certain subsidiaries, including Fidelity Management & Research Company (FMR Co.) and Fidelity Management & Research (Canada) ULC (“FMR-Canada”) – which carries on business in British Columbia as FMR Investments Canada ULC; and ii) Fidelity Investments Canada ULC (“FIC”) and its affiliates. Fidelity Management & Research (Canada) ULC (“FMR‑Canada”) commenced business in Ontario on February 1, 2018. FMR-Canada is registered as a portfolio manager with the Ontario Securities Commission (“OSC”) and as a portfolio manager with the other Canadian securities commissions. The scope of FMR‑Canada’s business is currently limited to offering the Global Asset Allocation (“GAA”) strategies through a discrete portfolio management team at FMR‑Canada. The GAA strategies are offered by FMR-Canada on a sub-advised basis to accounts advised by Fidelity Investments Canada ULC (“FIC”), with FMR-Canada acting as either direct sub-adviser to FIC or as sub-sub-adviser through non-Canadian Fidelity advisers, including (and principally) US SEC-registered investment advisers, such as FMR Co., Inc. (“FMRCo”). FMR-Canada does not offer these strategies directly to investors in Canada. FMR-Canada has also registered “Fidelity Investments” as a trade name in Canada.

The statements contained herein are based on information believed to be reliable and are provided for information purposes only. Where such information is based in whole or in part on information provided by third parties, we cannot guarantee that it is accurate, complete or current at all times. It does not provide investment, tax or legal advice, and is not an offer or solicitation to buy. Graphs and charts are used for illustrative purposes only and do not reflect future values or returns on investment of any fund or portfolio. Particular investment strategies should be evaluated according to an investor’s investment objectives and tolerance for risk. Fidelity Investments Canada ULC and its affiliates and related entities are not liable for any errors or omissions in the information or for any loss or damage suffered.

© 2026 Fidelity Investments Canada ULC. All rights reserved. Fidelity Investments is a registered trademark of Fidelity Investments Canada. The presenter is not registered with any securities commission and therefore cannot provide advice regarding securities.

INM 4465472 07/26 4482901-v2026626