Introduction to DeFi

Meghan Chen, MFE, CFA | Digital Assets Strategist

Written: July 2022

Note that since this article was written, Ethereum successfully completed the transition to proof-of-stake consensus on September 15, 2022.

This article is Part 2 of a five-part series that aims to provide an overview of the Ethereum network from an investment perspective. The first part provides some background on the mechanics of Ethereum, and then outlines its general value proposition and competition positioning. The second, third and fourth parts each focus on a key aspect of the ecosystem of applications that may be built on Ethereum, and aim to provide insight with regard to use cases, growth metrics and considerations. The fifth part examines the future of Ethereum from a broader perspective, and includes a discussion of its development roadmap, as well as different types of risks that may be associated with an investment in ether.

Introduction

Decentralized finance (DeFi) applications currently make up a major part of applications on Ethereum. DeFi is a blockchain-based alternative to traditional financial services. It provides a financial ecosystem that does not rely on centralized intermediaries such as banks, brokerages and exchanges to offer products and services. DeFi applications enable a host of use cases, including borrowing and lending, asset exchange and asset management. The smart contracts that underlie DeFi applications are transparent and auditable. DeFi services aim to be available 24/7.

The table below provides an overview of the current main types of DeFi protocols and their counterparts in CeFi and traditional finance. CeFi, which stands for centralized finance, refers to centralized platforms that bridge DeFi/crypto and traditional finance.

| DeFi | CeFi | Traditional finance | |

|---|---|---|---|

| Asset exchange | Decentralized exchanges (e.g., Uniswap, Curve) |

Crypto exchanges (e.g., Coinbase, Kraken) |

Traditional exchange and brokers |

| Lending and borrowing | Crypto decentralized lending platforms (e.g., Aave, Compound) |

Crypto centralized lending platforms (e.g., BlockFi, Genesis) |

Commercial banks and non-bank lenders |

| Asset management | Crypto decentralized portfolios (e.g., Yearn, Convex) |

Crypto asset managers (e.g., Grayscale, Galaxy Digital) |

Traditional asset management firms |

DeFi vs. traditional finance

The table below illustrates key potential advantages of DeFi compared to traditional financial services.

| DeFi | Traditional finance |

|---|---|

Anyone can examine the protocol’s code and see how it works. Flow of funds into and out of protocols is publicly visible. |

Operations are based on internal decisions taken within financial institutions. |

DeFi is permissionless to use and services are resistant to censorship. |

Users need to apply for services. Accounts with financial institutions can be frozen, and transactions can be blocked. |

Users can choose to keep custody of their own money. |

Users rely on companies to custody their money. |

Users can easily transfer assets across DeFi protocols and interact with various protocols using a single wallet. |

Accounts with financial institutions are siloed. Financial institutions keep their own internal records. Transfers between platforms can take days. |

Transaction activity is pseudonymous, allowing better privacy. |

Financial activity is generally tied to the identity of users. |

Note: The above illustrates potential advantages only. Actual advantages may or may include aspects listed above. Blockchain is still an emerging technology, and it remains to be seen the long-term advantages it may bring. Please note there are also potential disadvantages of DeFi (see “Considerations” at the end of this article). The characteristics of traditional finance depicted above may help hinder criminal activity such as money laundering, terrorist financing, financing of illegal activities, etc.

In addition, DeFi potentially allows for more value accrual to users, as there are no centralized intermediaries that can extract economic rents.

Case studies

Uniswap

Decentralized exchanges (DEXs) are blockchain-based counterparts of centralized exchanges, allowing users to swap assets, but requiring no centralized intermediaries to facilitate trading. Uniswap is an open-source decentralized exchange protocol built on Ethereum that offers trading services for various fungible tokens on the Ethereum blockchain. ERC-20 is the Ethereum token standard for fungible tokens.

Instead of using an order book, as traditional exchanges do, Uniswap operates through liquidity pools. Each Uniswap smart contract manages a liquidity pool made up of reserves of two ERC-20 tokens. Anyone can provide liquidity to a pool by depositing an equal value of each token. In return, liquidity providers receive tokens representing their share of the pool, which can be used to redeem their share of the pool’s assets at any time. When traders use a pool to complete an exchange, they pay a fee which goes (at least in part) to the liquidity providers of that pool. As the ratio of assets in the pool changes due to trading activity, exchange prices are adjusted accordingly based on a deterministic algorithm. Liquidity providers bear certain risks associated with the volatility of exchange prices.

Uniswap has been developing and adding features over time. The first version of Uniswap launched in November 2018, and only allowed users to trade ERC-20 tokens with ETH. The second version, launched in May 2020, added ERC-20/ERC-20 liquidity pools. In May 2021, the third version was launched, introducing multiple fee tiers, as well as new options to allocate liquidity within a certain price range. DEXs have been growing in popularity over the past couple of years. In May 2022, Uniswap said that it had processed $1 trillion in lifetime trading volume.1

Aave

Aave is an open-source protocol that allows users to earn interest on deposits and borrow assets with a variable or fixed interest rate. Aave is available on Ethereum, as well as some other blockchain networks, including Avalanche, Fantom and Harmony.

Lenders deposit funds into liquidity pools, and users can borrow from these pools. The deposit yield and borrowing rate vary depending on the asset transacted. Depositors into Aave’s pools receive a corresponding amount of tokens that represent their holdings in the pool. Borrowers on Aave must provide enough collateral to back up their loan. All loans are overcollateralized, meaning that the value of the collateral must be higher than the loan amount. The collateralization ratio depends on the asset used as collateral. If the loan value rises above a certain percentage of the collateral, the loan is defined as under-collateralized and may be liquidated.

Aave has a history of innovation in the DeFi space. In 2020, Aave pioneered the concept of flash loans, which contributed to the platform’s rise in popularity. Flash loans are loans that are borrowed and repaid within the same block, and are largely used to capture arbitrage opportunities. In January 2022, Aave Arc, a permissioned liquidity pool designed for institutions, was launched. Institutions that wish to join the liquidity pool must undergo KYC and anti-money laundering procedures.

Aave, like Uniswap, is governed via a decentralized autonomous organization, with the AAVE token serving as the platform’s governance token (see Part 4 – Introduction to DAOs ).

Growth of DeFi

The chart below shows the total value of user funds deposited in DeFi protocols (total value locked, or TVL) over time. TVL dropped significantly in the second quarter of 2022, reflecting a general drop in cryptocurrency prices. In addition to macroeconomic pressures on risk assets, the collapse of the Terra blockchain in May following the de-pegging of the UST stablecoin, as well as insolvency concerns regarding multiple CeFi companies, contributed to the crypto bear market during this period. Despite this, DeFi TVL has grown significantly over the past couple of years. Ethereum is currently the market share leader by TVL.

FIGURE 1: DeFi TVL over time and by blockchain

Stablecoins

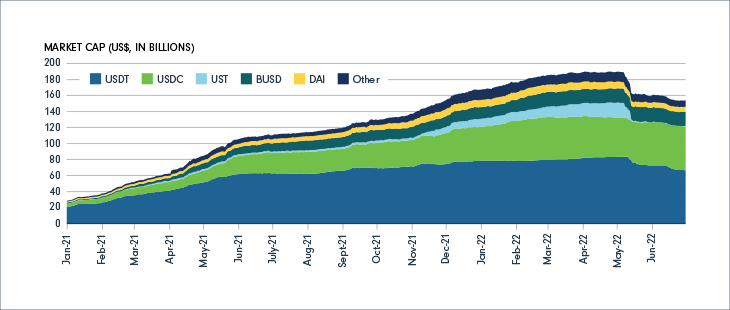

Stablecoins are cryptocurrencies that aim to peg their price to that of another asset, such as a fiat currency or a commodity such as gold. Most major stablecoins are pegged to the U.S. dollar. Stablecoins can serve as a bridge between fiat currencies and digital currencies on blockchains, serving as on- and off-ramps for liquidity purposes. They are also widely used as collateral on, and to provide liquidity to, various DeFi protocols. Along with the growth of DeFi, the market capitalization of stablecoins has grown significantly over the past couple of years.

FIGURE 2: Stablecoin market cap over time

The table below summarizes the major types of stablecoins.

| Type | Description |

|---|---|

| Fiat-backed | Stablecoins are backed by fiat reserves held by a centralized institution. The number of stablecoins in circulation is proportional to the amount of fiat reserves. |

| Crypto-backed | Stablecoins are backed by other cryptocurrencies locked into smart contracts as collateral. Generally, there is overcollateralization to provide a buffer against volatility in the crypto assets used as collateral. |

| Algorithmic | Stablecoins are not backed by fiat or crypto collateral. Aims to achieve price stability via algorithms that manage the supply of tokens in circulation. |

Note: The above represents current major categories of stablecoins and is not an exhaustive list of all possible types of stablecoins.

Currently, the largest stablecoins by market cap, USDT and USDC, are both fiat-backed. Because major stablecoins play an important role in the DeFi ecosystem, their collapse could have contagion effects on the wider crypto market. Further regulation and the existence of a diverse set of stablecoins may help mitigate the risks.

Considerations

DeFi remains relatively unestablished compared with traditional finance. DeFi applications may require a certain level of technical knowledge to understand and use, which may present a hurdle from an adoption standpoint. As Dapps are based on the execution of smart contract code, it is imperative that implemented code is robust to withstand faults and vulnerabilities. Historically, however, many DeFi protocols have had their vulnerabilities exploited, resulting in the loss of significant amounts of user funds. According to Chainalysis, over $2 billion was stolen from DeFi protocols in 2021.2 In addition, many investors have lost funds in scams such as “rug pulls,” where developers build what appear to be legitimate crypto projects before disappearing with investors’ money. Chainalysis indicates that rug pulls took in more than $2.8 billion worth of cryptocurrency from victims in 2021, and that rug pulls are commonly seen in DeFi.3 Increasing investor familiarity with DeFi, more robust due diligence processes and better crypto-related crime detection techniques may mitigate these issues in the future. Also, there is still a great deal of regulatory uncertainty regarding DeFi, in connection with aspects such as securities law, taxation policy, etc.