Factor investing: A data-driven investment strategy

Index investing has been gaining popularity with investors, but did you know there’s a more rule-based, evidence-driven way to build a portfolio? It’s a strategy, rooted in research that professionals have used for decades, known as factor investing.

Let’s break down what it is, why it matters and how it can be used to make more strategic investment decisions.

So what is factor investing?

Factor investing is an investment strategy that uses data and research to select investments like stocks and bonds based on characteristics known as “factors.” These factors are measurable traits that have been shown to improve returns over the long term. Rather than relying on guesswork or market timing, factor investing applies these insights in a consistent and disciplined way. Think of it like building a sports team: traditional index investing is like picking the most popular players (index funds) or drafting a few star athletes (individual stocks). Factor investing, on the other hand, is like using data and player statistics to choose players based on specific measurable traits, such as speed, strength or consistency, that have historically led to performance. Certain traits may produce better outcomes in different scenarios, and the range of different style factors will behave differently as business cycles change and regimes evolve.

There are two common types of factors we consider in investing.

- Macro factors: These factors help explain risk and return across asset classes and include broad economic factors like inflation, interest rates and economic growth.

- Style factors: These factors help explain risk and return within asset classes and are measurable characteristics of individual securities, such as value, momentum or size.

Fidelity leverages style factors across a number of ETF products to drive outcomes.

Dividend yield: Focuses on stocks that pay higher-than-average dividends.

Value: Seeks stocks that seem underpriced compared with their true worth (value).

Momentum: Investing in stocks that have performed well over the recent past.

Quality: Investing in companies with strong balance sheets and profitability.

Low volatility: Exposure to stocks with lower risk than the broader market, as well as stable earnings.

Size: Focuses on smaller companies (small-cap stocks) that may offer higher growth potential.

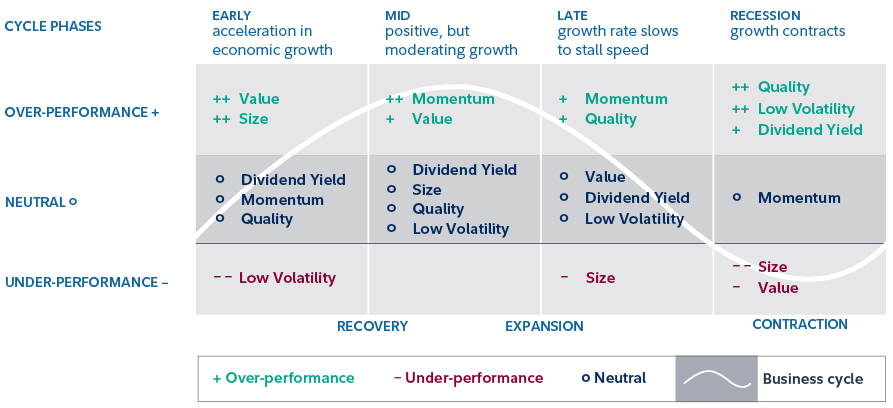

Certain factors can have better outcomes in different market environments.

Why should investors care?

You don’t have to be a professional investor to benefit from factor investing. Today, anyone can access these strategies affordably through ETFs to invest in a smarter, more consistent way. Benefits include

- Higher potential returns: Some factors have historically outperformed the market over the long term.

- Diversification: Factors behave differently in various market conditions.

- Transparency: Factor-based ETFs often follow clear, rules-based methodologies.

How to use factors in a portfolio

There are three common ways to apply factor investing.

Strategically: Use factors to establish strategic exposure. Some factors have been found to outperform the market over time, so using a strategic buy-and-hold approach may improve long-term benefits.

Tactically: Tilt your portfolio toward certain factors based on where we are in the business cycle. For example, factors like low volatility and quality often do well during recessions, while other factors like value and size tend to outperform during the early part of the business cycle.

For portfolio construction: Using factors for portfolio construction is like taking a multivitamin. Many of us don’t get all our vitamins from our diet, and you may take multivitamins to fill a gap. Factors can be used for portfolio construction in a similar way. For example, an investor's current portfolio may be deficient in generating dividend income compared with the broader market. In that scenario, the investor could make an allocation to a high-dividend factor strategy to fill that gap. Investors could also combine factor strategies to create core portfolios that are diversified, creating a smoother investment journey.

Whatever your goals, factor investing is a powerful strategy that can be used as a building block to enhance any portfolio.

Ready to learn how factor investing can work for you?

To learn more about Fidelity factor ETFs, visit fidelity.ca/factorinvesting.