TFSA basics

Regardless of what you are saving for, a Tax-Free Savings Account (TFSA) is a great way to save for any financial goal – a long-term goal such as retirement or a short-term goal such as a car or a vacation.

Did you know: if you’ve never opened a TFSA, you can contribute up to $109,000 today?*

What is a TFSA? A TFSA is a flexible investment account, offering tax-free earnings and withdrawals, which can help you grow your savings and reach your investment goals faster.

Numbers to know

$0

Taxes you'll pay on TFSA earnings

$7,000

2026 TFSA contribution limit

$109,000

Maximum TFSA contribution limit*

Since 2009, TFSAs have represented a unique way for Canadians to save money and pay less tax. Any Canadian resident with a social insurance number who has reached the age of majority in their province could open a TFSA and save up to $6,000 every year until 2023, when the contribution limit increased to $6,500. In 2024, the contribution limit increased again to $7000.* They are called “savings accounts,” but TFSAs can hold many different types of investments, including all Fidelity Funds.

To get the most out of a TFSA, it should be part of your overall financial plan.

How TFSAs can help achieve investment goals

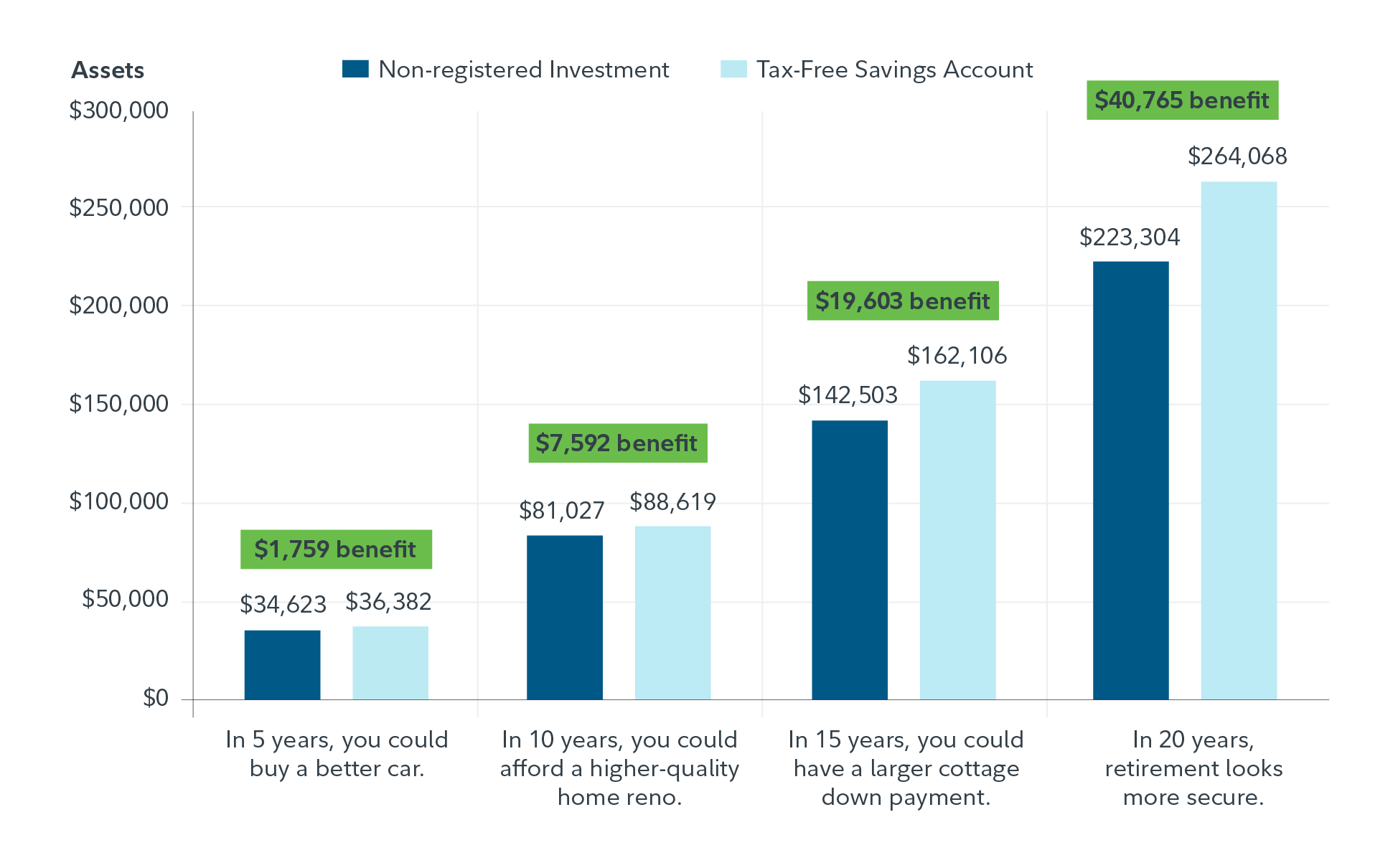

There are two ways a TFSA can help you grow your savings faster than an ordinary savings account or a non-registered investment.

Whether you’re saving for a car, a house, a cottage or a comfortable retirement, the additional savings benefit of a TFSA can be significant in both the short and long term. The following table illustrates the difference between savings in a TFSA compared with non-registered investment over five-, ten-, 15- and 20-year periods.

Assumptions: Rate of return of 6%, marginal tax rate of 50% for interest and 25% for capital gains, distributions reinvested, distribution yield of 2.0%, distribution composed of 50% interest and 50% capital gain, initial contribution of $6,000 and contributions increase in $500 increments based on a 2% inflation rate. Contributions were made at the beginning of the period. Unrealized capital gains were taxed at the end of the holding period. This assumption ignores contributions from prior years.

Six key TFSA facts

- Every year, your TFSA has contribution room limits. Since 2009, the Canadian government has set a maximum amount that qualified Canadians can contribute to their TFSA every year, regardless of income.

- Unused TFSA contribution room can be carried forward indefinitely to future years. If you didn’t contribute the maximum amount in a given year, you’re allowed to “catch up” in the future, within the overall limits of your TFSA contribution room limits.

- At any point, if you contribute more than the total allowed contribution limit, the over-contribution amount will be subject to a tax penalty.

- Withdrawals are not considered as taxable income and will generally not trigger government benefit clawbacks or affect tax credits.

- Any withdrawals from your TFSA are added to your TFSA contribution room limit in the following year, so you can recontribute the amount you withdrew in a future year.

- You can have more than one TFSA, but be careful that your combined accounts do not create an over-contribution; you cannot over-contribute without a tax penalty. You can check your TFSA contribution limits by going to the CRA website and logging in to My Account.

TFSA contribution limit by year from 2009 to 2026

The following chart shows the contribution limits for each year that the TFSA has been available.

| Year | Contribution limit |

| 2009 | $5,000 |

| 2010 | $5,000 |

| 2011 | $5,000 |

| 2012 | $5,000 |

| 2013 | $5,500 |

| 2014 | $5,500 |

| 2015 | $10,000 |

| 2016 | $5,500 |

| 2017 | $5,500 |

| 2018 | $5,500 |

| 2019 | $6,000 |

| 2020 | $6,000 |

| 2021 | $6,000 |

| 2022 | $6,000 |

| 2023 | $6,500 |

| 2024 | $7,000 |

| 2025 | $7,000 |

| 2026 | $7,000 |

| Total | $109,000 |

Choosing between a TFSA and an RRSP

If you are looking to save in the most tax-efficient way, TFSAs and RRSPs can both be an effective option to achieve your savings goals. However, each plan has its own distinctive features. RRSPs can be an excellent complement to your TFSA.

|

TFSAs | RRSPs |

|---|---|---|

| What is the primary purpose? | Short-term general savings or long-term retirement savings | Retirement savings |

| Are contributions tax-deductible? | No | Yes |

| Are contributions made with after-tax dollars? | Yes | No, contributions are made with pre-tax dollars |

| What is the tax treatment of earnings inside the account? | Tax free | Tax deferred |

| Can I make a withdrawal at any time? | Yes | Yes, but withdrawals are taxed as income |

| Is there tax on withdrawals? | No | Yes, but withdrawals are taxed as income |

| Do withdrawals increase contribution room? | Yes1 | No |

| Does unused room carry forward? | Yes | Yes |

| Is there an age limit? | No | Yes, must convert to a RRIF or life annuity by age 71 |

| Do income attribution rules apply? | No | Generally no, but may apply to withdrawals from a spousal RRSP |

| Do withdrawals affect income-tested government benefits and tax credits? | No, generally withdrawals are not included in taxable income | Yes, generally withdrawals are included in taxable income |

| What is the contribution room limit/formula? | $7,000 per year regardless of income (2026) plus available TFSA contribution room | 18% of earned income to a maximum of $33,810 (2026), plus unused RRSP deduction room |