Bond prices, rates and yields

When investing in bonds, it’s important to understand how prices, rates and yields affect one another.

If you buy a new bond and plan to keep it to maturity, changes in prices, interest rates and yields typically do not affect you, unless the bond is called. But investors don’t have to buy bonds directly from the issuer and hold them until maturity; instead, bonds can be bought from and sold to other investors on what’s called the “secondary market.” Bond prices on the secondary market can be higher or lower than the face value of the bond, because the current economic environment and market conditions will affect the price investors are actually willing to pay for the bond. And the bond’s yield, or the expected return on the bond, may also change.

How price is measured

Price is important when you intend to trade bonds with other investors. A bond’s price is what investors are willing to pay for an existing bond.

Bond prices are generally quoted in terms of percentage of face (par) value.

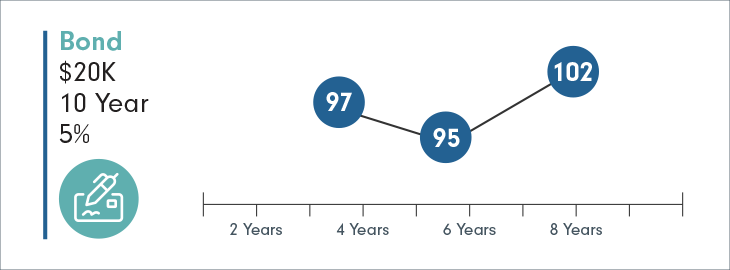

Example: You are considering buying a corporate bond. It has a face value of $20,000. At three points in time, its price – what investors are willing to pay for it – changes from 97, to 95, to 102. (Note: This is how bond prices are generally quoted – as a percentage of the face (par) value – indicating investors are willing to pay 97%, 95% or 102% of the face (par) value at various points in time. The same convention is used in the examples below as well.)

Price and interest rates

The price investors are willing to pay for a bond can be significantly affected by prevailing interest rates. If prevailing interest rates are higher than when the existing bonds were issued, the prices on those existing bonds will generally fall. That’s because new bonds are likely to be issued with higher coupon rates as interest rates increase, making the old or outstanding bonds generally less attractive, unless they can be purchased at a lower price. So higher interest rates mean lower prices for existing bonds.

If interest rates decline, however, the prices of existing bonds usually increase, which means an investor can sometimes sell a bond for more than the purchase price, since other investors are willing to pay a premium for a bond with an interest payment, also known as a coupon, that is higher.

Buyers will generally want to pay less for a bond whose coupon rate is lower than prevailing interest rates. Conversely, buyers will generally be willing to pay more for a bond whose coupon rate is higher than prevailing interest rates.

This relationship can also be expressed between price and yield. The yield on a bond is its return expressed as an annual percentage, affected in large part by the price the buyer pays for it. If the prevailing yield environment declines, prices on those bonds generally rise. The opposite is true in a rising yield environment; in short, prices generally decline.

Example: Price and interest rates

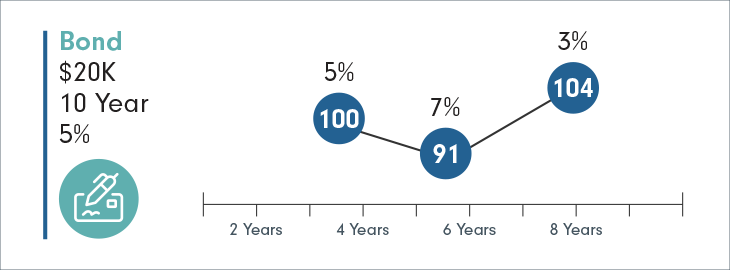

Let’s say you buy a $20,000 corporate bond with a coupon rate of 5%. While you own the bond, the prevailing interest rate rises to 7% and then falls to 3%.

1. When the prevailing interest rate is the same as the bond’s coupon rate, the price of the bond is 100, meaning that buyers are willing to pay you the full $20,000 for your bond.

2. Prevailing interest rates rise to 7%. Buyers can get around 7% on new bonds, so they’ll only be willing to buy your bond at a discount. In this example, the price drops to 91, meaning they are willing to pay you $18,200 ($20,000 x .91).

3. The prevailing interest rate drops to 3%. Buyers can only get 3% on new bonds, so they are willing to pay extra for your bond, because it pays higher interest. In this example, the price rises to 104, meaning they are willing to pay you $20,800 (20,000 x 1.04).

More factors that affect price

Financial health of the issuer

The financial health of the company or government entity issuing a bond affects the coupon that the bond is issued with: higher-rated bonds issued by creditworthy institutions generally offer lower interest rates, while less financially secure companies or governments will have to offer higher rates to attract investors.

The creditworthiness of the issuer will also affect the bond’s price on the secondary market. If the issuer is financially strong, investors are willing to pay more, since they are confident that the issuer will be capable of paying the interest on the bond and pay off the bond at maturity. But if the issuer encounters financial problems – and especially if it’s downgraded by one of the ratings agencies (see “ Bond ratings”) – investors may become less confident in the issuer. As a result, the price of its bonds may fall.

The risk that the financial health of the issuer will deteriorate, known as credit risk, increases the longer the bond’s term to maturity. As a result, bonds with longer maturities also tend to pay more, in order to compensate investors for the additional risk.

Inflation

Inflationary conditions generally lead to a higher-interest-rate environment. Therefore, inflation has the same effect as interest rates. When the inflation rate rises, the price of a bond tends to drop, because the bond may not be paying enough interest to stay ahead of inflation. Remember that a fixed-rate bond’s coupon rate is generally unchanged for the life of the bond.

The longer a bond’s maturity, the more chance there is that inflation will rise rapidly at some point and lower the bond’s price. That’s one reason bonds with a long maturity offer somewhat higher interest rates: they need to do so to attract buyers who otherwise would fear a rising inflation rate. That’s one of the biggest risks incurred when you agree to tie up your money for, say, 30 years.

Minimizing bond price confusion

Bond pricing involves many factors, but determining the price of a bond can be even harder because of the way bonds are traded. Because stocks are traded throughout the day, it’s easier for investors to know at a glance what other investors are currently willing to pay for a share. But with bonds, the situation is often not so straightforward.

Prices on statements may not be what you paid

The price you see on a statement for many fixed-income securities, especially those that are not actively traded, is a price that is derived by industry pricing providers, rather than the last-trade price (as with stocks).

The derived price takes into account factors such as coupon rate, maturity and credit rating. The price is also based on large trading blocks. But the price may not take into account every factor that can affect the price you would be offered if you actually attempted to sell the bond.

Derived pricing is commonly used throughout the industry.

Most bonds are not listed

Most bonds are not listed on an exchange. Of the hundreds of thousands of bonds that are registered, only a few thousand are generally available on an exchange on any given day. These bonds will be quoted with an offered price, the price the dealer is asking the investor to pay. Canadian government and corporate bonds are more frequently also listed with bid prices, the price investors would receive if they’re selling the bond. Less-liquid bonds, such as provincial bonds, are rarely quoted with a dealer’s bid price.

If the bid price is not listed, you must receive a quote from a bond trader.

Yield

Yield is the anticipated return on an investment, expressed as an annual percentage. For example, a 6% yield means that the investment averages a 6% return each year. There are several ways to calculate yield, but whichever way you calculate it, the relationship between price and yield remains constant: the higher the price you pay for a bond, the lower the yield, and vice versa.

Current yield is the simplest way to calculate yield:

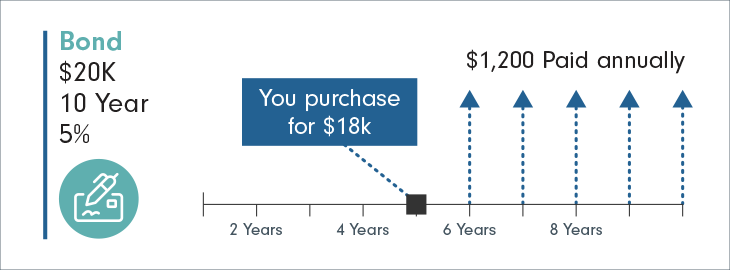

For example, if you buy a bond paying $1,200 each year and you pay $20,000 for it, its current yield is 6%. While current yield is easy to calculate, it is not as accurate a measure as yield to maturity. The yield to maturity in this example is around 9.25%.

Yield to maturity

Yield to maturity is often the yield that investors inquire about when considering a bond. Yield to maturity requires a complex calculation. It considers the following factors.

- Coupon rate: The higher a bond’s coupon rate, or interest payment, the higher its yield. That’s because each year the bond will pay a higher percentage of its face value as interest.

- Price: The higher a bond’s price, the lower its yield. That’s because an investor buying the bond has to pay more for the same return.

- Years remaining until maturity: Yield to maturity factors in the compound interest you can earn on a bond if you reinvest your interest payments.

- Difference between face value and price: If you keep a bond to maturity, you receive the bond’s face value. The actual price you paid for the bond may be more or less than the face value of the bond. Yield to maturity factors in this difference.

For example, say a bond has a face value of $20,000. You buy it at 90, meaning that you pay 90% of the face value, or $18,000. It is five years from maturity.

The bond’s current yield is 6.7% ($1,200 annual interest / $18,000 x 100).

But in this case the bond’s yield to maturity is higher. It considers that you can achieve compounding interest by reinvesting the $1,200 you receive each year. It also considers that when the bond matures, you will receive $20,000, which is $2,000 more than what you paid.

Yield to call

Yield to call is the yield calculated to the next call date, instead of to maturity, using the same formula.

Yield to worst

Yield to worst is the worst yield you might experience, assuming the issuer does not default. It is the lower of yield to call and yield to maturity.

Yields vs. interest payments

It is possible that two bonds having the same face value and the same yield to maturity nevertheless offer different interest payments. That’s because their coupon rates may not be the same.

If you are purchasing a bond primarily for a regular stream of income, don’t just pay attention to the yield to maturity, but note the coupon rate, as that will determine how much money you actually receive each year.

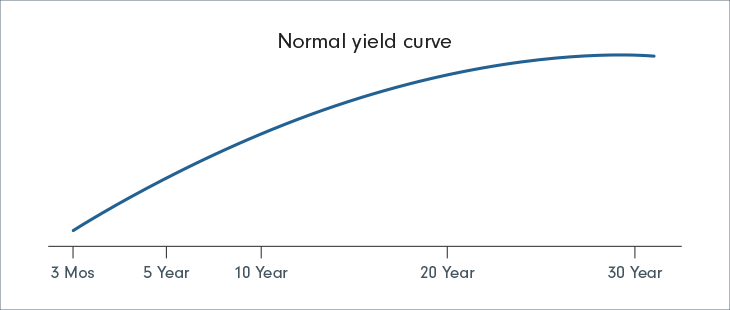

Yield curve and maturity date

A yield curve is a graph demonstrating the relationship between yield and maturity for a set of similar securities. A number of yield curves are available. Two that investors commonly consider are the U.S Treasury yield curve and the Canadian yield curve.

The shape of a yield curve can help you decide whether to purchase a long-term or short-term bond. Investors generally expect to receive higher yields on long-term bonds. That’s because they expect greater compensation when they loan money for longer periods of time. Also, the longer the maturity, the greater the effect of a change in interest rates on the bond’s price.

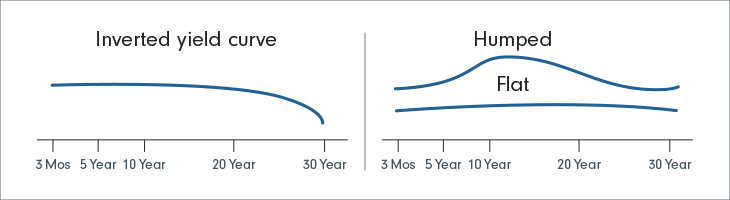

Normal or ascending yield curve

A “normal” yield curve (also called a positive or ascending yield curve) means that the yield on long-term bonds is higher than the yield on short-term bonds. This is historically very common, since investors expect more yield in return for loaning their money for a longer period of time.

Other yield curves

Other yield curves are possible, when long-term yields are not higher than short-term yields. These may make you reconsider whether to purchase a long-term bond.